|

Mortgage Rates at All-Time Lows

As many of you have heard or taken advantage of already, mortgage rates have recently dropped to all-time lows. The COVID-19 pandemic and demands have been quite interesting to say the least, but we appreciate everyone’s patience for what lenders are faced with today and we’re comparing our large network of wholesale lenders daily for the best client options. Capacity is a challenge across the board due to demands, but extended locks on refinances apply where needed and now is a great time to consider reviewing the numbers.

We’ve tried to be proactive to update all, but due to demands as you can imagine we’ve defaulted to more reactive for those that need the update, quotes, that may benefit, etc. and put in order. Purchase transactions also are prioritized over refinances due to contractual commitments, but understandable. There is a good chance that the ‘majority’ of you will benefit from refinancing or at least considering it and watching where rates trend through the rest of this year and into 2021.

Is it time to get a quote or refinance? We can run a quote for you by contacting us (thanks for your patience again) – and comparing our network of wholesale lending partners. If you don’t wish to extend loan term you can choose any fixed term between 8-30 years on conventional loans.

Contact us:

- If you have a 30 year conforming conventional rate around 3.875% or higher

- If you have a 20 year fixed conventional rate around 3.75% or higher

- If you have a 15 year fixed conventional rate around 3.625% or higher

- If you have a VA or FHA rate at or above 3.25%

- If you’re trying to remove PMI, or refinance out of FHA to conventional

- If you’re considering shortening your term

- If you’re considering cash-out for home improvements or debt consolidation, paying off a second mortgage, etc.

|

|

|

|

|

|

Oregon Real Estate Market

|

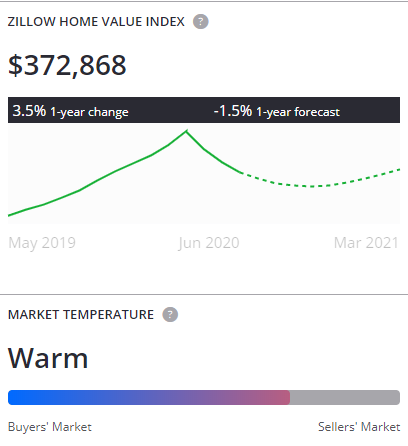

The median home value in Oregon is $372,868. Oregon home values have gone up 3.5% over the past year and Zillow predicts they will fall -1.5% within the next year. The median list price per square foot in Oregon is $218. The median price of homes currently listed in Oregon is $378,900 while the median price of homes that sold is $359,600. The median rent price in Oregon is $1,850.

Foreclosures will be a factor impacting home values in the next several years. In Oregon 1.1 homes are foreclosed (per 10,000). This is lower than the national value of 1.2

Mortgage delinquency is the first step in the foreclosure process. This is when a homeowner fails to make a mortgage payment. The percent of delinquent mortgages in Oregon is 0.6%, which is lower than the national value of 1.1%. With U.S. home values having fallen by more than 20% nationally from their peak in 2007 until their trough in late 2011, many homeowners are now underwater on their mortgages, meaning they owe more than their home is worth. The percent of Oregon homeowners underwater on their mortgage is 4.1%.

Source: Zillow

|

Washington Real Estate Market

|

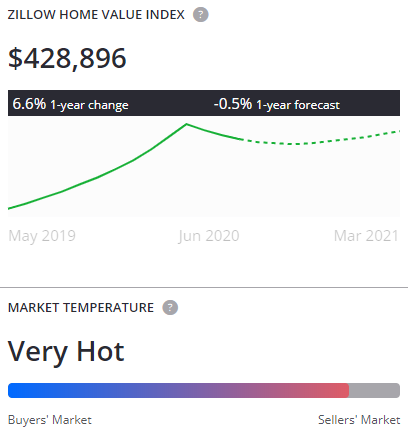

The median home value in Washington is $428,896. Washington home values have gone up 6.6% over the past year and Zillow predicts they will fall -0.5% within the next year. The median list price per square foot in Washington is $237. The median price of homes currently listed in Washington is $415,000 while the median price of homes that sold is $408,400. The median rent price in Washington is $1,995.

Foreclosures will be a factor impacting home values in the next several years. In Washington 0.8 homes are foreclosed (per 10,000). This is lower than the national value of 1.2

Mortgage delinquency is the first step in the foreclosure process. This is when a homeowner fails to make a mortgage payment. The percent of delinquent mortgages in Washington is 0.6%, which is lower than the national value of 1.1%. With U.S. home values having fallen by more than 20% nationally from their peak in 2007 until their trough in late 2011, many homeowners are now underwater on their mortgages, meaning they owe more than their home is worth. The percent of Washington homeowners underwater on their mortgage is 4.3%.

Source: Zillow

|

Pacific NW Housing Market:

2008 Financial Crisis vs. 2020 COVID-19 Crisis

|

We get this question often being on the front lines of the housing market crash of 2008 as well as where we are today. What are the similarities? In our opinion, there are few. While this pandemic has created a significant financial impact on many American families, it’s simply not the same as it was nearly a decade ago.

We have to remember leading into the financial crisis for many years up until 2008, there were billions of terrible mortgage loans originated. These subprime loans had little oversight as it pertained to the qualifications of borrower and ability-to-repay, income analysis, credit, and financial reserves. In addition, most were done on short-term adjustable rates with added pre-payment penalties, with little to no skin in the game on down payment. Income (ability-to-repay new mortgage debt) was simply made up and hardly verified with not only some applications, but one could argue the majority of applications at times. What this created was an artificial demand in housing, created by many that could not sustain variable payments or volatility, that ultimately would burst. If you have not seen it, we highly suggest watching The Big Short which paints an accurate picture of what led up to the housing bubble that undoubtedly would pop.

One could imagine with thousands of US Homeowner’s not only carrying, but requiring these subprime loans to even qualify for a home, what happens when liquidity and lending dries up overnight. Not only is demand completely gone, but defaults significantly rise with no option to refinance or restructure (even with the attempted loan modifications that were a disaster). This was a messy recipe, primarily to the artificial rise in housing prices and equity. As we know, this led to records in new short-sales and foreclosures that lasted for years. Everyone was impacted in some way or another if it were equity or assets.

Leading into this ‘shorter-term’ (we hope) COVID-19 Pandemic has been much different. We’ve had a thriving stock market, housing market (in most areas), and economy prior to this. More importantly a significant change in ability-to-repay requirements and tedious income and asset verification for all consumers buying a home and qualifying for new home financing. While some new questionable programs are entering the market, all require ‘skin in the game’ and most are conservative fixed rate agency-backed (Fannie Mae, Freddie Mac, Ginne Mae) loan programs. Most require some form of minimum down payment and all require specific debt-to-income ratio guidelines and very thorough income review and analysis. More consumers today have a stronger ability to retain home and make their mortgage payments. In addition, the CARES Act offered temporary forbearance assistance for those that truly needed it to defer mortgage payments (not meant for those that can continue to make) to avoid foreclosure or other issues.

Many are seeking unemployment benefits or slowly returning back to work during a global pandemic (as we hope shorter-term) versus global financial crisis (impacting long-term). We know many are still negatively impacted of course and we hope for a quick vaccine, positive news, and safety/recovery for all. The media we understand is extreme on both sides and while we don’t agree with fear or ignorance, the data speaks for itself in the housing market. Buyers are significantly active, we’re seeing bidding wars on most every listing today (many price points and due to lower inventory), and demand will continue and GROW the rest of 2020 and beyond from our vantage point. Mortgage rates are at ‘historic’ lows making affordability greater and pending home sellers may see motivation to help increase inventory and buy that next home with rates so low and this opportunity. The Pacific NW Housing Market is doing very well as are the majority regarding equity protection. Unless something drastically changes economically, we see a healthy NW housing market in the foreseeable future (even if any short temporary dips here and there in certain areas of the market).

|

Vantage Mortgage Group, Inc.

Oregon’s #1 Mortgage Broker

|

Thank you to all of our clients and business partners for making VMG Oregon’s #1 Mortgage Broker in 2019 (and beyond) as well as being in the Top 100 Brokers in the United States! We have led the way since 2007 to go against the industry rhetoric and special interests. We have and will remain to be independent and put our clients before lenders, forcing competition every day for better execution and loan terms from the top wholesale lending partners. We’re on pace to help over 1,000 local families in the Pacific NW in 2020 and will continue to adopt new technology and embrace the average 17 years’ of experience our team members have to offer.

We appreciate each and every one of you and the support of our local small business and what that means to all of us and our local economy. We will always embrace facts and math, and expose the sales or marketing influences that don’t use either and instead steer a retail lender, special interests, and omitting the fiduciary duty (on the same exact agency-backed loans) to work for the consumer or Veteran only on new home purchase or refinance.

|

Thank you for your ongoing referrals for anyone you hear that may be in the market to buy or refinance (or simply need a second opinion).

|

|

|

|

|

|